In the initial years of a home loan, the interest component in equated monthly instalments (EMI) is larger, which gradually decreases as time goes on. Financial advisors recommend prepaying the home loan earlier as the money you prepay goes straight towards reducing the home loan principal and cutting the total interest cost.

Now, home loan rates are around 9 percent for many. So, borrowers are feeling the heat from increased costs.

The decision to prepay your home loan should be a well thought one. We will discuss here with an example the best time to do so and explain a couple of strategies to prepay the home loan.

Home loan repayment

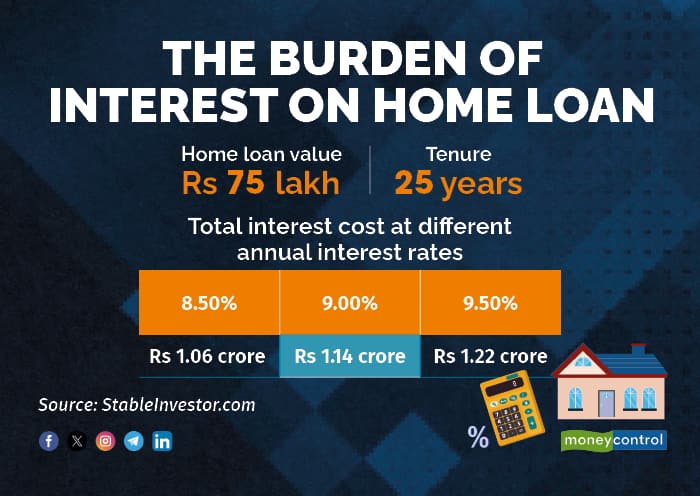

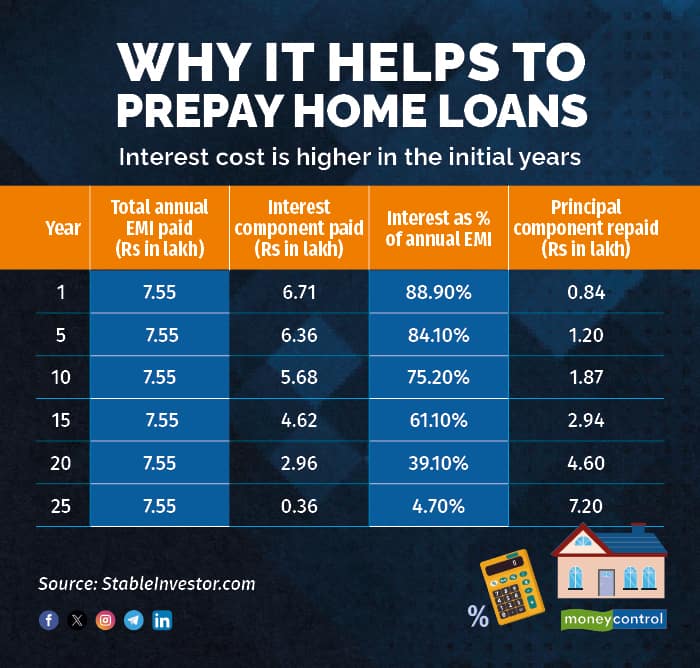

Assume you have a home loan of Rs 75 lakh for 25 years at a 9 percent rate of interest. You will be paying an EMI of Rs 62,940 per month. During the term of 25 years, you will repay the principal of Rs 75 lakh plus interest of Rs 1.14 crore. It means if you keep your loan outstanding for the entire 25-year tenure you will end up paying at least double the loan amount (refer to graphic).

Interest component is high in the initial years

In the initial years of loan repayment, a major part of your EMI goes towards interest, while a small part goes towards principal repayment.

Have a look at the annual loan amortisation schedule for your loan of Rs 75 lakh, 25 years tenure and 9 percent interest rate (refer to graphic).

In the first year, 89 percent of EMIs go towards interest servicing and 11 percent of the Rs 7.55 lakh annual EMI (12 x Rs 62,940) goes towards principal repayment. In the 10th year, the interest component reduces to 75 percent and further down in the 15th and 20th year, it’s down to 61 percent and 39 percent, respectively.

So, every month, the interest component in the EMI decreases a bit while the principal repayment part rises. Here, the monthly EMI still remains the same.

“The bulk of EMI in the initial years is for interest servicing. And it is for this very reason that you should consider prepaying the home loan during the initial years,” says Dev Ashish, founder of StableInvestor.com.

Here are a couple of home loan pre-payment strategies:

Use your bonus well. Pay an extra EMI every year

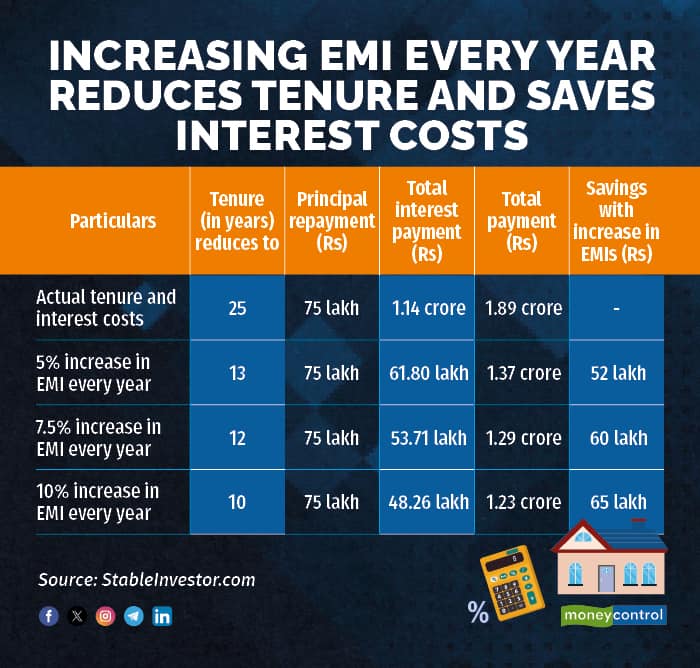

Here, instead of 12 EMIs of Rs 62,940 every year, you should pay 13 EMIs of this amount. This pre-payment strategy will bring down your tenure from 25 years to about 19-20 years. You will also end up saving around Rs 32 lakh in interest costs.

“Every year you might get some bonus/incentives from your employer. So, a part of that surplus can be used to make at least one extra EMI payment,” says Ashish. He adds that if making one full additional EMI payment is difficult, then just paying Rs 5,000 extra EMI per month will have a similar impact.

In addition to annual bonuses and surpluses, you can also liquidate low yielding investments such as traditional endowment policies that fetch 5-6 percent annual returns over the long term or even fixed deposits. Do not withdraw from your Employees Provident Fund (EPF) and National Pension Scheme (NPS) corpus for home loan prepayment. “Doing so could set your retirement planning back by years,” says Adhil Shetty, CEO, Bankbazaar.com.

Increasing EMI by 5-10 percent every year

Another option is to increase your EMI, in line with your annual increments, and direct surpluses towards the home loan. Many borrowers successfully pre-pay their loans with tenures of over 25 years within 10-12 years.

So, as your yearly income grows, your monthly EMI for a home loan should also be increased. Say in this example, if you increase your EMI by just 5 percent, your 25-year loan gets over in just 13 years. You will end up saving around Rs 52 lakh in interest costs by just increasing the EMI by 5 percent every year (refer to graphic).

“Five percent is not too big a payment and better than not prepaying at all. It allows you to prepay slowly and leaves you money to invest for goals such as saving for retirement and educating your children,” says Shetty.

And if you increase the EMIs by 7.5 percent and 10 percent every year, then your loan gets over in 12 years and 10 years, respectively. Here, you will save Rs 60 lakh and Rs 65 lakh by increasing the EMI by 7.5 percent and 10 percent every year respectively.

Avoid using emergency fund for loan prepayment

Emergency funds should be used during job loss and medical emergencies in the family.

“Using emergency funds for making prepayments can force borrowers to avail loans at higher interest rates or redeem other investments at suboptimal prices for meeting unforeseen expenses during periods of unemployment,” says Ratan Chaudhary, Head of Home Loans, Paisabazaar.

Do not redeem investments meant for crucial financial goals

Just because it is beneficial to prepay your home loans, it doesn’t mean you sell your investments to generate the cash. If your equity mutual funds earn you, say 12 percent compounded returns over a period of time, and your loan runs at 8 percent, it doesn’t make sense to sell a high yielding asset to pay off an 8 percent loan.

Besides, investments are — and should be — earmarked for long-term goals. Any premature withdrawals from your investments would make it harder for you to reach your financial goals. “And it may also force you to borrow costlier loans to achieve your crucial financial goals,” Chaudhary warns.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!