The new tax regime, with minimal exemptions, has done away with the over 70 tax breaks that the old regime had offered. However, some key tax benefits find a space in the new tax regime's scheme of things as well. For instance, the minimal exemptions regime retains the tax exemption on employers' contribution to employees' National Pension System (NPS) of up to 10 percent (14 percent in the case of government employees) of basic pay plus dearness allowance, if any.

More awareness needed

While the NPS has seen its popularity as a reliable retirement planning solution grow over the years, the fact is that the tax benefits the scheme offers remain the chief draw for many subscribers.

Yet, not many maximise the tax breaks that the NPS has to offer. If your employer contributes up to 10 percent of your basic salary to your NPS corpus, it is exempt from tax. However, employees have been less-than-enthusiastic about signing up for this arrangement.

In an interview with Moneycontrol in June 2023, Pension Fund Regulatory and Development Authority (PFRDA) chairman Deepak Mohanty had pointed out that NPS’ coverage happens to be limited at present, despite the huge potential. “We have onboarded around 13,000 corporates, but the take-up rate by the employees is quite low,” he said.

Here’s all that you need to know about how you can gain if your employer contributes to your NPS account.

NPS’ tax deductions

If you contribute voluntarily to NPS under the All Citizens’ Model that is open to all Indian citizens over 18 years of age, you can claim deductions under section 80C provided you choose the old tax regime.

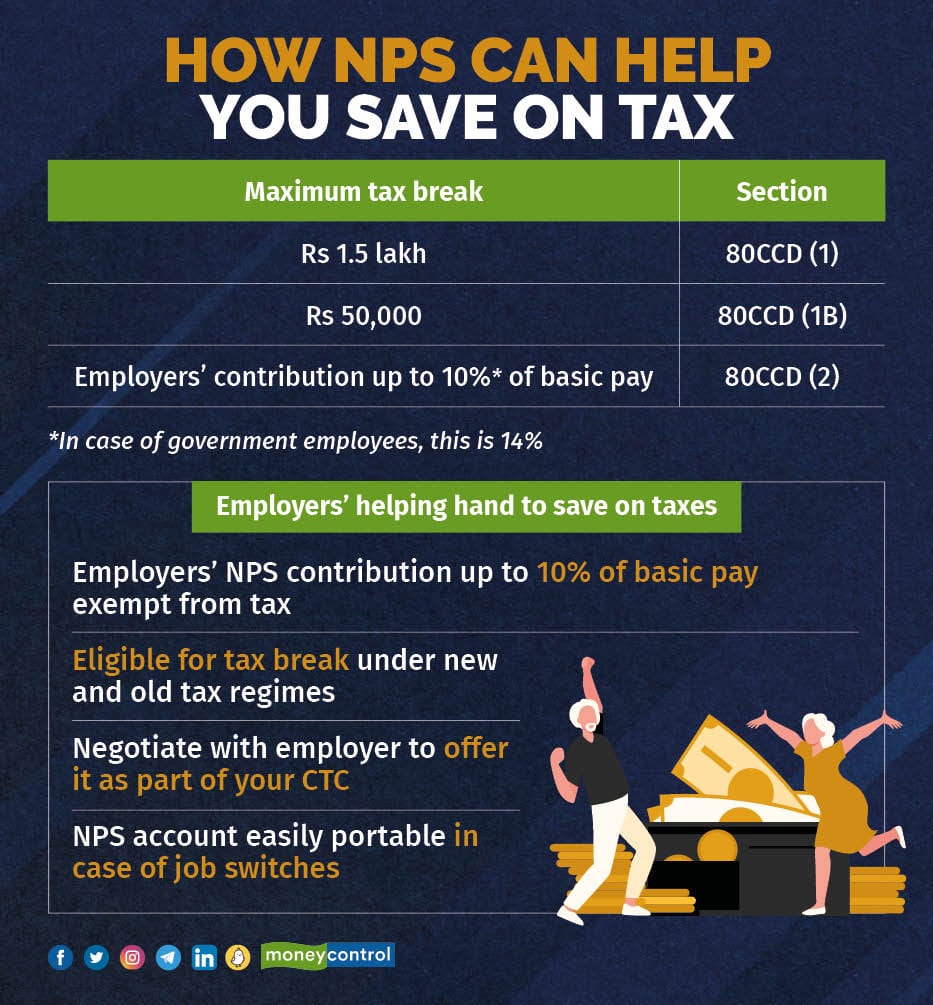

As an employee, your contributions of up to 10 percent of your basic salary plus dearness allowance will qualify for deductions under section 80CCD (1). You can also contribute to NPS as an individual too without having to be an employee of an organisation. However, the deductions under this section cannot go beyond the overall 80C limit of Rs 1.5 lakh. This apart, you can claim an additional break of Rs 50,000 under section 80CCD (1B). These two benefits are generally well-known.

However, the tax benefits offered under the corporate scheme remain underutilised due to lack of awareness. Section 80CCD (2) can help you cut your tax outgo substantially if your employer contributes to your NPS corpus. This benefit is available in both old and new tax regimes.

Indian employees - resident Indians, non-resident Indians (NRIs), and overseas citizens of India (OCI) – aged between 18-70 years can register as NPS subscribers under the corporates scheme through their employers. If you are already registered as an NPS subscriber, you can also share your permanent retirement account number (PRAN) with your employer to route the contributions through this facility.

Also read: The 25-35 age group accounts for the largest number of NPS subscribers, shows PFRDA report

So, if you are a salaried employee and your cost-to-company structure is such that your employer contributes to your NPS, you will be eligible for a deduction of up to 10 percent of your basic salary (basic plus dearness allowance). If you happen to be a government employee, this deduction will be even higher at 14 percent. Your own contributions will continue to be eligible for deduction under section 80CCD (1) and 80CCD (1B).

Complementary to EPF contribution

Do note that your employer can contribute to your NPS over and above the employees’ provident fund (EPF) contributions. Employees or employers need not to choose one over the other.

As an employee, you can transfer the account that is tagged to a permanent retirement account number (PRAN) to another employer when you switch jobs, provided the new employer is willing to contribute to your NPS. Depending on your employer’s policy, NPS investment management charges, custodian fees, transaction charges, and so on will have to be borne either by you or the employer.

Mandatory for government employees

NPS is mandatory for all central government employees who joined the workforce after January 1, 2004, except the armed forces. Most state governments, too, have adopted it. Private organisations – that is, employers – also qualify for tax benefits on account of contributions to employees’ NPS.

Employers’ contribution of up to 10 percent of employees’ basic salary is treated as a business expense and allowed as a deduction from their profit and loss account under section 36(1)(iv)(a) of the Income Tax Act.

Organisations registered under the Companies Act, 2013 or registered co-operative societies are allowed to contribute to their employees’ NPS. Government and affiliated organisations, too, can adopt the corporate model, besides public sector enterprises. Registered partnership firms, proprietary concerns, and certain foreign companies (for eligible Indian employees) are also eligible.

The rules of withdrawal

NPS withdrawal rules remain the same – at the age of 60, you can withdraw 60 percent of the corpus as a lump sum. The balance of 40 percent has to be mandatorily used to purchase annuities, which will be used to pay your pension post-retirement.

You can make partial withdrawals of up to 25 percent of your own contributions after three years in case of certain critical illnesses, purchase of property, children’s education, and so on.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!