When the Employees’ Provident Fund Organisation (EPFO) announced an interest rate of 8.25 percent for the financial year 2023-24 (higher than 8.15 percent for 2022-23 and 8.1 percent in 2021-22) on February 10, the good news didn’t just end there.

Not only is this be applicable to employees’ contribution of 12 percent of their basic salary and their employers’ matching contribution but also to any additional contribution they make voluntarily.

Also read: Voluntary Provident Fund: Here’s how you can increase your retirement corpus

How VPF works

Put simply, Voluntary Provident Fund (VPF) is an extension of your EPF account. It gives you a chance to save more for your retirement. Your employers have to mandatorily deduct 12 percent from your basic salary (and dearness allowance, if any) every month as your EPF contribution.

Your employer has to contribute an equal amount to your provident fund corpus. Now, out of your employer’s contribution, 8.33 percent (subject to a maximum basic pay of Rs 15,000, or Rs 1,250) is directed towards your employees’ pension scheme (EPS) account.

Your VPF contribution can go up to 100 percent of your basic pay. Besides interest rate, even withdrawal, maturity and taxation rules are identical to that of EPF.

Also read: How to choose the right tax-saver 80C investments before the March 31 deadline | Simply Save

If you wish to invest in VPF, go through your employers’ policies and figure out the process to inform your administration or human resources (HR) regarding your intention to make additional contributions. Many employers offer online facilities to enable VPF contributions. You will not have to open a fresh account or complete any know-your-customer (KYC) process.

Depending on your employers’ VPF framework, you could either specify the amount or proportion of your basic salary that should be deducted from your salary, to be invested in your EPF account. You can, equally easily, also turn the tap off before the cut-off dates mentioned by your employers. Do note, however, that some employers may not allow you to make VPF contributions at the end of the financial year. In such cases, you will not be able to opt for this route this financial year.

VPF contributions are eligible for deductions under section 80C, within the overall limit of Rs 1.5 lakh. However, if your total provident fund (EPF plus VPF) contributions in a financial year exceed Rs 2.5 lakh, the interest earned on the ‘excess’ amount is taxable.

VPF’s edge over other fixed-income avenues

If your goal is retirement planning, VPF is a must-have in your portfolio. “From a long-term, retirement planning perspective, it is the best instrument available today. Salaried individuals should make the most of it instead of looking at bank recurring deposits.

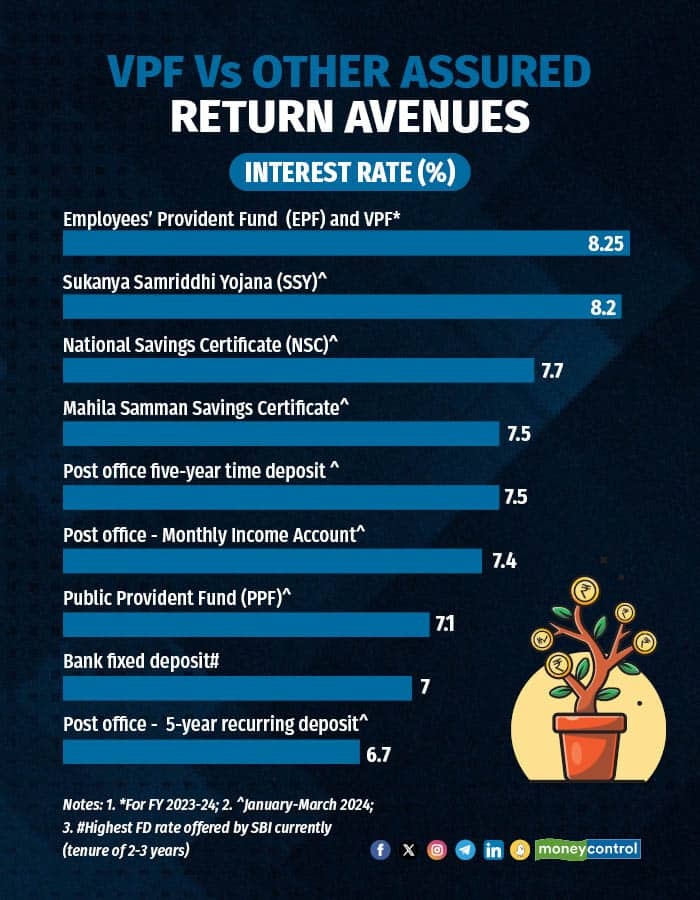

Considering the interest rate of 8.25 percent and sovereign guarantee that it carries, no other fixed income even comes close,” says Kalpesh Ashar, Founder, Full Circle Financial Planners and Advisors. Amongst small savings schemes (see graphic), for instance, the highest rate of return is offered by Sukanya Samriddhi scheme currently, and at 8.2 percent, it is slightly lower than EPF's interest rate for FY 2023-24.

Why EPF and VPF score over other fixed income instruments

Why EPF and VPF score over other fixed income instruments

Senior citizen savings scheme (SCSS), which offers interest rate of 8.2 percent and higher fixed deposit interest rates for senior citizens have not been taken into account, as yet-to-retire VPF subscribers will not be eligible for those offerings.

On the flip side, this reduces your cash flows over time, in simple words, your take-home pay. “You can look at a large allocation to VPF only as long as it does not pinch your cash flows,” he adds.

At retirement, you will get your entire corpus (EPF + VPF) back. Till then, your money is locked. However, the EPFO rules allow you to prematurely make partial withdrawals from your corpus for specific purposes such as house purchase, children’s education, treatment of critical illnesses, unemployment and so on. “Such instruments can be part of debt allocation in your portfolio but best suited solely for retirement as these are fairly illiquid,” says Dev Ashish, SEBI-registered investment advisor and Founder, Stable Investor.

If you are investing with your retirement goal in mind, he recommends investing across VPF, PPF and NPS (National Pension System). “(Out of your total intended retirement oriented investments) you can invest the initial Rs 2.5 lakh in EPF/VPF, the next Rs 1.5 lakh in PPF and the balance amount can be directed towards NPS,” says Dev Ashish.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!